You’re ready to sell your investment property but hesitant to pay capital gains taxes. You’ve heard about a 1031 exchange, yet the process and its rules seem complex or confusing.

If this sounds familiar, you’re not alone. Many first-time exchangers feel uncertain about the requirements for identifying and acquiring replacement properties. While a 1031 exchange may appear complicated at first glance, with the right guidance, the rules are straightforward and manageable.

In this article we’ll cover the important rules of a 1031 exchange across three categories, including:

- Replacement Rules

- Identification Methods

- Timelines

Replacement Rules

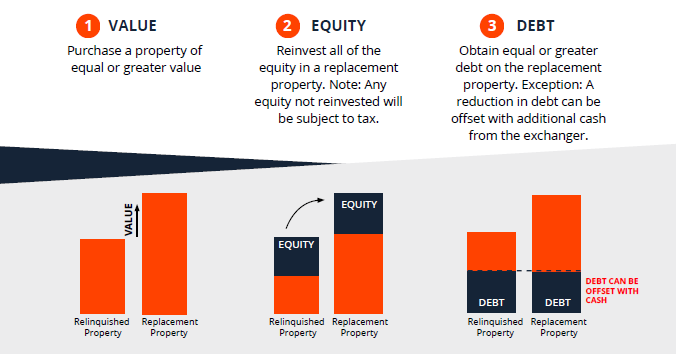

The power of a 1031 exchange lies in its ability to defer capital gains taxes when reinvesting in new real estate. To ensure full tax deferral, the IRS requires that the value, equity, and debt from your relinquished property be properly reinvested.

In most cases, you’ll want to purchase a replacement property of equal or greater value than the one you sell. This not only preserves the tax deferral but also allows you to “trade up” and grow your real estate portfolio.

Equity

To fully defer capital gains taxes, you must reinvest all net equity from the sale into the replacement property. Any portion not reinvested—called “boot”—will be taxable.

Example:

If you sell a property with $100,000 in equity and reinvest the full amount, you defer all capital gains taxes. However, if you reinvest only $70,000, the remaining $30,000 will be subject to tax.

Debt

Most property sales involve financing, so debt also plays a role. Generally, you must replace equal or greater debt on your new property. A reduction in debt can be offset by contributing additional cash.

Example:

If your original property carried $200,000 in debt, your replacement property should include at least $200,000 in financing—or, alternatively, $150,000 in debt plus $50,000 in cash.

Identification Methods

If you’ve read our article on how a 1031 exchange works, you know that the identification period has strict deadlines that must be followed. To meet those deadlines, it’s important to understand the rules surrounding identifying replacement properties.

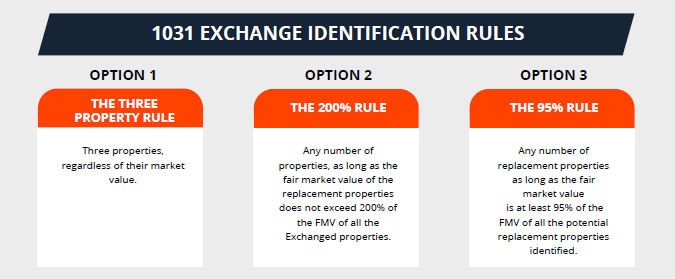

THREE (3) PROPERTY RULE

There are three ways to identify a replacement property, the most common way being the three-property rule. As the name suggests, this rule allows you to identify up to three (3) properties during the identification period, regardless of their market value. Once the identification period is over, these will be the properties that you are allowed to purchase as a part of the 1031 exchange.

The Three Property Rule is the preferred strategy used by 1031 exchangers.

200% RULE

This rule allows you to identify any number of properties, as long as their total (aggregate) fair market value (FMV) of all identified properties does not exceed 200% of the FMV of the total (aggregate) net sales value of the property(s) you are selling.

For example, if the value of the property you are selling is $100,000, under this rule you would be allowed to identify up to $200,000 (200%) of replacement properties. This rule is commonly preferred by investors wishing to diversify their portfolio.

If you aim to diversify your investment portfolio and plan on acquiring four or more properties, the Three Property Rule will not be enough. Moreover, if you are uncertain about your preferences for a replacement property, you can select several properties (with fair market values within the 200% allowance) and then take extra time to decide.

For those who wish to diversify their portfolios identifying more than 3 properties, the 200% rule is preferred.

95% RULE

The third method is the 95% rule. Under this rule, you are allowed to identify any number of replacement properties so long as the FMV of the properties you purchase by the end of the 1031 exchange have a value of at least 95% of the FMV of all the properties you identified.

For example, if the total FMV of all the properties you identified is $200,000, you must purchase at least $190,000 worth of property for the 1031 exchange to be conducted successfully. This rule is typically used when both the three-property rule and the 200% rule fail to meet the investor’s needs.

Investors may have a need to identify more than three properties and more than 200% of the sales value of the relinquished property. In this case, the 95% rule is best.

Remember, if you do not acquire and close on at least 95% of the value of the identified like-kind replacement properties, the entire 1031 exchange transaction will be disallowed.

Timelines

If you’ve read our article on how a 1031 exchange works, you know that the identification period has strict deadlines that must be followed. To meet those deadlines, it’s important to understand the rules surrounding identifying replacement properties.

45-Day Identification Rule

Once the sale of your property is complete, the identification period of the 1031 exchange process begins. This period is relatively short and has a strict timeline that will prevent you from completing a successful exchange if not met.

You have 45 days after the sale of your property to identify a suitable replacement property (or properties) that qualify under the like-kind requirement. This 45-day period starts the day after the sale closes and includes all calendar days, including weekends and holidays.

For example, if you sell your property on June 1st, you will have until July 16th to identify a replacement.

180-Day Close Rule

After identifying a suitable replacement property, the next important step is to complete a purchase. You have 180 days after the sale of your original property to close on a new one, so time is again of the essence in this stage. If it takes you the full 45 days to identify a suitable property during the identification period, you will have 135 days left to close.

At closing, the QI will release the funds they have been holding in escrow from the sale of your relinquished property. If you are purchasing multiple properties, you may have multiple closings, so long as they all fall within the 180-day window.

After the closing is complete, not only will you now be the owner of a new property and have successfully completed your 1031 exchange, but you will have deferred some or all of the capital gains tax you normally would have had to pay.

Things to Note:

- There are no extensions for the weekends or holidays that fall within your identification period.

- 1031 exchange language must be written in the sales contract when selling your property outlining the QI which whom the funds will be sent to upon closing.

- Exchangers must never take constructive receipt of the sales proceeds to qualify for a valid 1031 exchange.

- Replacement properties that you are considering must be sent to your Qualified Intermediary (“QI”) and identified no later than midnight of the 45th calendar day

- If 1031 exchange investors do not identify within the 45-day ID period, the 1031 exchange becomes disqualified.

- Identified properties must be acquired within 180 days following the close of the relinquished property to qualify for a valid 1031 exchange following the close of your relinquished property sale transaction.

- Only properties sent to the Q.I. for ID will qualify for 1031 exchange.

- A Qualified Intermediary (QI) must provide a written and signed document that describes the properties you wish to identify including legal description, street address, or name of property or DST (if applicable).

- If you wish to revoke a replacement property recently identified, you must provide a written and signed document that describes the property that you wish to remove from the list of identified properties.

Conclusion

We hope this article has given you a good overview of what the 1031 exchange rules are and how to better navigate your next exchange. While the IRS rules surrounding a 1031 exchange can seem detailed, they are manageable with proper planning and professional guidance.

Understanding the replacement, identification, and timing requirements is key to completing a successful exchange and maximizing your tax deferral benefits. Although a 1031 exchange can be complicated, they are a powerful tool that every real estate investor should have in their toolkit.

If you are considering a 1031 exchange for your property or have additional questions about the process, don’t go it alone. Our experts at 1031 Qualified Intermediary have helped countless investors navigate the 1031 exchange process and we would love to assist you as well.https://1031qualifiedintermediary.net/#form

📅 Ready to get started? To see whether a 1031 exchange is right for you, call (888) 245-1031, email info@1031qualifiedintermediary.net or schedule a consultation with one of our experts today.

Download your free copy of “The Power of 1031 Exchanges” to learn more about how 1031 exchanges can complement your portfolio.